Specialising in multi-country payroll solutions

- Real, knowledgeable people providing accurate employment advice

- Fast, responsive and reliable service with robust SLAs

- Supporting every step of the employee lifecycle - from hire to retire

Your guide to seamless global expansion

- Centralised account management with a single point of contact

- Access local HR & payroll experts in every location

- Onboard new global talent in days not weeks

Trusted advisors supported by technology

- A dedicated team of employment experts to take care of all your needs

- A single, global tech platform for all your hiring requirements

- Easy-to-use tech platform that integrates with your existing HR software

”With TopSource we were able to have employees hired or maintained in Nutreco without having to establish an entity in these countries for only 1-2 employees. I think most countries are covered by TopSource, so they can help us with almost all cases. Good advice on conditions and direct contact with employees. Invoicing done directly to the company. An easy process compared to hiring employees by ourselves.”

Annette van Duijnhoven

Nutreco

"We searched the market for a local payroll vendor in 2014 and we chose TopSource as our partner. We were looking for error free and timely payroll processing and TopSource Worldwide delivers this, saving us time and money. We have worked together for 8 years now and would recommend them to anyone.”

Praveen Lihinar

Sungard Availability Services India Pvt Ltd

Employ and pay anywhere, any way you want

Global EOR

Global EOR

Complete employment contracts and management of employee benefits through our established entities. We handle compliance and the entire hiring & onboarding process from payroll to termination where required.

Global & Local Payroll

Global & Local Payroll

Fully compliant, consolidated payroll processing for globally dispersed teams - with enhanced local payroll services in countries such as India and the UK.

Global Entity

Global Entity

Want to set up a local entity in another country? Already have foreign entities and want help managing them and keeping them compliant? Whatever stage you’re at, we can help you every step of the way.

Global Advisory

Global Advisory

Sorting out the right way to hire employees and expand abroad means you need experts on your side. We can work with you to ensure compliance no matter how you expand.

Global EOR

Global EOR

Complete employment contracts and management of employee benefits through our established entities. We handle compliance and the entire hiring & onboarding process from payroll to termination where required.

Global & Local Payroll

Global & Local Payroll

Fully compliant, consolidated payroll processing for globally dispersed teams - with enhanced local payroll services in countries such as India and the UK.

Global Entity

Global Entity

Want to set up a local entity in another country? Already have foreign entities and want help managing them and keeping them compliant? Whatever stage you’re at, we can help you every step of the way.

Global Advisory

Global Advisory

Sorting out the right way to hire employees and expand abroad means you need experts on your side. We can work with you to ensure compliance no matter how you expand.

Countries that we support

0+

countries covered

0+

employees

0+

clients

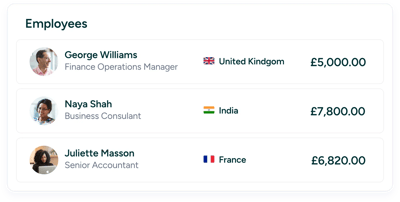

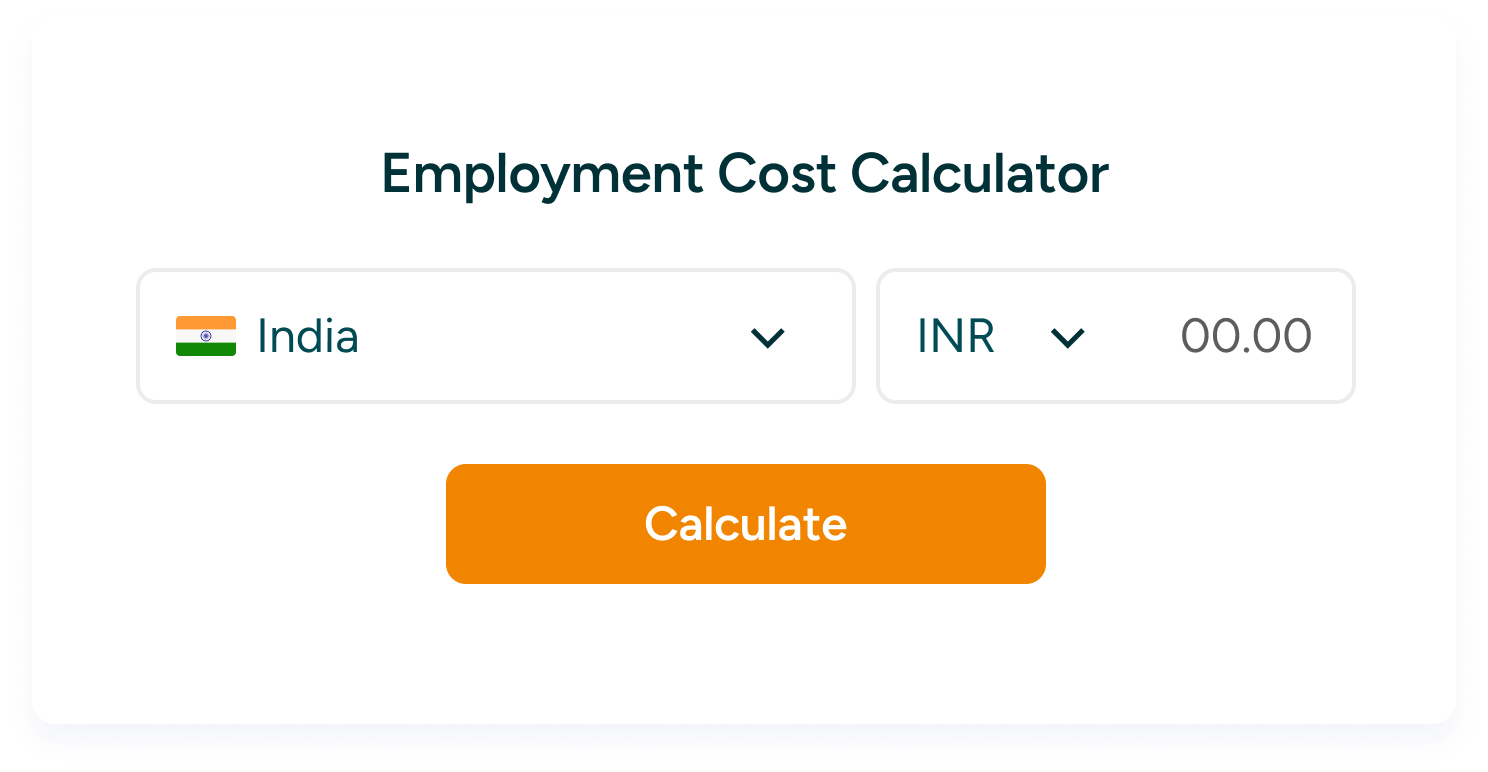

Employee Cost Calculator

Get a precise estimate of how much a potential global hire may cost each month.

Discover how TopSource Worldwide can help you grow your global team